Now entering the third quarter of 2020, small business owners across the nation hope to jump start their businesses. We have seen various impacts due to the coronavirus pandemic, but the question is… Is it over? What will it take for the economy to rebound and how might a second wave change things?

Some industries like the online food ordering/delivery industry and the data storage/internet services industry[1] have seen increased demand for products or services, while other industries like the tourism, sports, restaurant and retail industries[2] have taken big hits.

In this article, we take a brief look at some of the most common economic metrics to determine the pandemic’s economic impact, how the economy has reacted to widespread shutdowns, and what the rest of 2020 could look like.

Economic factors to consider

The most common measures of economic health are GDP (gross domestic product); unemployment rate; inflation rate and consumer prices; and interest rates. Consumer confidence also plays a vital role in the health of the economy.

GDP is “the monetary value of all finished goods and services made within a country during a specific period,” typically one year.

GDP can be a good measure of how much product a nation or region is producing, and therefore how healthy a nation’s economy is. However, the GDP metric fails to account for the value of under-the-table employment, volunteer work, and household production, which can be significant in certain areas.

So how is the economy doing right now?

The coronavirus pandemic and resulting economic recession has escalated to be among the top 3 worst global recessions in the last century, topping the Great Recession of 2008-2009[3], the other two being the two World Wars. Many experts predict that a swift recovery will take place, but we may start to see a few unique trends in response to the pandemic. Let’s take a look at how the economy has reacted.

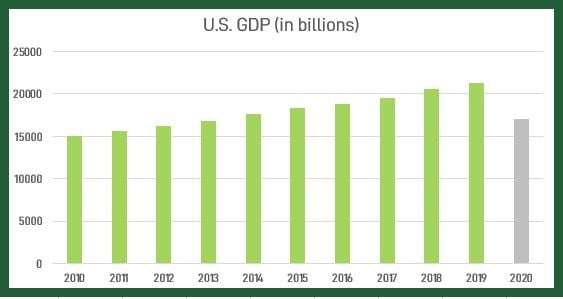

GDP

The U.S. Current-dollar GDP (not considering exchange rate, not adjusted for inflation) reached $21.43 trillion in 2019, with an increase of 4.1 percent over the 2018 number, according to the Bureau of Economic Analysis. But with the pandemic hitting the economy hard in the first half of 2020, Trading Economics predicts that 2020 will reach only $17 trillion, a number not seen since 2013. See Figure 1.

Recession is one thing. Recovery is another. This economic recession, usually measured by GDP gains or losses, is expected to be short. The economic recovery, however, could take years. Experts predict that it may take anywhere from 3-10 years for the economy to recover to pre-coronavirus levels.[4] But remember, the economy ebbs and flows in a natural cycle. Before coronavirus, the U.S. was experiencing the longest economic surge on record.[5] The pandemic is a major setback, but it is unlike the financial crisis of the Great Recession because it's from an outside force, and experts predict a faster recovery.

Figure 1 [source]

Unemployment

The second quarter of 2020 has seen a staggering rate of unemployment. April numbers came in at 14.7 percent, and May at 13.3 percent. [6] See Figure 2. While the initial jobless claims have backed off, the unemployment rate is not expected to return to pre-coronavirus levels for some time. Although this number may seem ominous of a prolonged economic recession, there are many major companies looking to hire.[7] But remember, small businesses account for 99.7% of businesses in America.[8] More than anything, we hope to see recovery and growth in the small business arena.

Figure 2 [source]

Inflation Rate

When the economy is in good shape, the supply and demand of consumer goods is in a comfortable trajectory. But when we see a recession, that balance is thrown off and the government may try to bring some stability by attempting to control the inflation rate. See Figure 3.

"Inflation is simply a rise in the average price of goods and services in the macroeconomy." [9]

We have seen small businesses shuttered while large corporations continue to provide the same products. Historically, when the competition is erased, inflation tends to spike. Small businesses have struggled to adapt without the capital access of large corporations. But, small business owners have risen to the challenge, and the government and communities have supported our small businesses like never before. We need to continue supporting local small businesses so they can continue to provide their unique products and services that bring culture, flavor, and jobs to our home towns.

Figure 3 [source]

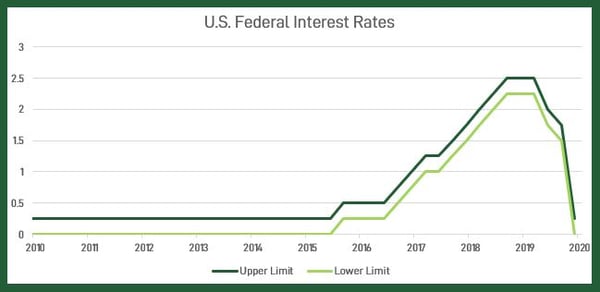

Interest Rates

After the Great Recession of 2008-2009, the Fed set interest rates near zero and took a new look at how to grow and keep the economy vibrant. It took several years for the interest rates to begin creeping back up. But when the coronavirus hit, that number again plummeted. See Figure 4. Because the Fed's benchmark interest rates directly influence bank interest rates, lowering the rate is meant to stimulate the economy and provide consumers with incentive to spend.

Figure 4 [source]

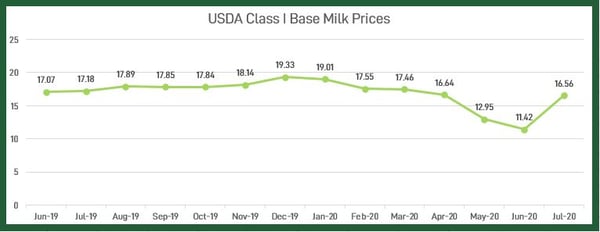

Milk Prices

And we'll throw this one in here, just for reference.

With the changes in demand across the nation when restaurants and schools closed their doors, the dairy industry saw a significant drop in milk prices. Dairy farmers saw a low of $11.42 per hundred-weight in June of 2020, but the crisis appears to be short-lived, although not entirely back to normal, with the base milk price returning to $16.56 for July. See Figure 5.

Figure 5 [source]

What are some projections for the remainder of 2020 and beyond?

The economic outlook for the remainder of 2020 is still unknown and largely riding on the reopening efforts of state and local governments. If cases continue to trend upward, as seen in recent data,[10] governors and local policy-makers may push pause or roll back on reopening plans, consequently dipping the economy into a longer recession.

What could a second wave (or revived first wave) of cases do to local economies? With contact tracing efforts and the rise in testing availability, health experts are better positioned to locate hotspots in specific regions. In light of that, local governments could have greater responsibility to advocate for and mandate policies for their localities. The economic downturn may not be as widespread, but we should still be vigilant in our efforts to keep our communities healthy.

Three Trends to Watch For Post-Coronavirus

1. Shifting Food Industry

Not only were restaurants and bars shuttered due to coronavirus, food supply chains were disrupted and created a phenomenon in which sometimes supply fell far short of consumer demand, but only because of limitations on the supply chain. In our own small town, dairy farmers faced a disrupted supply chain crisis where they had to dump some milk tanks. Restaurant owners scrambled to pivot their service to takeout and delivery, many of whom were successful, a trend that may continue in the years to come.

Many regular shoppers opted to shop online with online grocery services like Instacart and other retail giants like Walmart and Amazon rather than risk an infection at a grocery store location. But this was already a trend with major retailers before coronavirus, it only expanded a shift in retail/grocery services with companies who already had a head start with these developments.

2. Urban Exodus

There are a few reasons urban dwellers may be considering a move to more suburban or rural areas. First, America's cities have been rocked by the coronavirus pandemic as well as social and political protests, and so many people in the same place at the same time is a good place for a virus to run rampant. Getting away from risky environments may be a good incentive for people to consider a move to suburbia.

Second, and closely linked to the first, stay-at-home orders with nowhere to go may seem overwhelming and produce spikes in mental illness. Less populated areas with an abundance of natural resources would help people to stay healthy and moving, rather than staying at home watching Netflix.

And lastly, with so many people now working from home, employees may find that they do not want to give up their new lifestyle because of the extra time and family life it offers, and they may opt to continue working from home. Companies who employ office staff will need to shift their benefits to include work-from-home options in order to attract talent post-coronavirus.

3. Shifting Tourism Industry

Perhaps the industry that has been most affected by the coronavirus pandemic is the tourism industry. Fears of spreading the virus across state and country borders has halted tourism worldwide. While tourism is a big industry in the world's leading economies, some island countries rely heavily on tourism for a majority of their national economy. What will countries do about their loss of tourism revenue if the pandemic persists?

Some trends we may begin to see include virtual experiences, trade deals and logistics investment to expand product lines worldwide, and more local tourism with residents encouraged to explore their home countries.

At Gehman Accounting, we hope for big wins for small businesses who have been impacted. Here are a few suggestions for small business owners. 1) Think like entrepreneurs. How has the pandemic shifted demand and how can you meet your consumers where they are? 2) Rally your resources. What grants or loans might be available and how might a relationship with a business advisor boost your confidence? 3) Be unique. Are you identical to the company down the road? Stand out from the competition by pursuing a niche or unique identifier.

And to all the consumers, remember to shop local and support your local economy.

Topics: Recession- Coronavirus- Economy